Brexit: an overview

As we approach the end of the Brexit transition period on 31 December 2020, there are a number of changes that will affect the import and export of goods to and from the European Union (EU). These changes will inevitably have an impact on the operations of stakeholders in the supply chain, whether you are a driver, a haulage company, a freight forwarder, a customs intermediary or a port operator.

Import and export declarations will be required from 1 January 2021 regardless of whether a trade deal is agreed between the United Kingdom of Great Britain and Northern Ireland (UK) and the EU before the end of the transition period. The UK has published its plans to implement a three-phase approach concerning the import of goods from the EU to Great Britain (GB); this will follow a similar process to Rest of World goods. The EU has stated that it will not replicate the UK's phased approach where exports are concerned; therefore, full declarations will be required for all exports from GB to EU from 1 January 2021.

The phased import approach is detailed in the UK Government's Border Operating Model and will require a degree of thought for those stakeholders in the supply chain involved in the import of goods to GB. While for those importing standard goods it might provide a further period of respite, for those handling controlled goods or goods for which additional requirements apply, changes will be effective from 1 January 2021.

The Border Operating Model is broadly split into two sections: the Core Model and Additional Requirements. The Core Model will apply to all goods movements between EU and GB regardless of mode of transport. Additional requirements will apply only to specific goods movements, for example goods with Sanitary and Phytosanitary controls.

The Core Model

Importers and exporters will have to complete GB and EU customs declarations after the transition period. Certain locations will require lodgement of customs declarations prior to the movement of goods, which is likely to affect certain modes of movement, such as RoRo. Importers and exporters will need to ensure that any applicable customs duties on imports are paid under the new UK Global Tariff and on exports under the existing Combined Nomenclature. To achieve this, those involved in the customs declaration process will need to determine the origin, classification and customs value of the goods being shipped.

VAT is another important consideration. VAT will be levied on goods imported to GB from the EU following the same rates and structures as applied to Rest of World imports. From 1 January 2021, VAT registered importers might be able to use postponed VAT accounting. In practice, this means that UK VAT-registered persons/businesses will account for the import VAT on goods imported into the UK on their VAT returns. They will both pay and recover VAT on the same VAT return. This new measure will apply to goods imported from all countries, including the European Union. This amendment should mitigate cash flow concerns for businesses that are involved in the import of goods to the UK. It should be highlighted that non VAT-registered persons/businesses will have to pay VAT on goods through the customs processes at the time of import from 1 January 2021, however, these can be deferred using a Duty Deferment Account (DDA).

With a view to maintaining safety and security standards, declarations will be required for goods moved between GB and the EU. Declarations will involve the collation of more information on the goods and will serve to clarify who is importing what and how frequently.

Additional requirements

Additional requirements will only affect specific goods moved between GB and EU. For these movements, special certification will be required and goods may have to enter via specified locations and undergo additional checks at the frontier border. In practice, some of these additional requirements will occur before and/or after the Core Model processes. For goods moved from the EU to GB, these additional requirements will be introduced in stages; for goods being moved from GB to the EU, they will be introduced as of 1 January 2021.

Additional requirements are applicable to several categories of goods.

- Goods covered by international conventions/commitments. (CITES, Kimberley, ATA Carnets)

- Goods subject to sanitary and phytosanitary controls (animal products, fish, shellfish, and live animals).

- Goods with additional customs requirements (excise goods)

- Other goods including strategic exports (fire arms, bottled water, waste, controlled drugs)

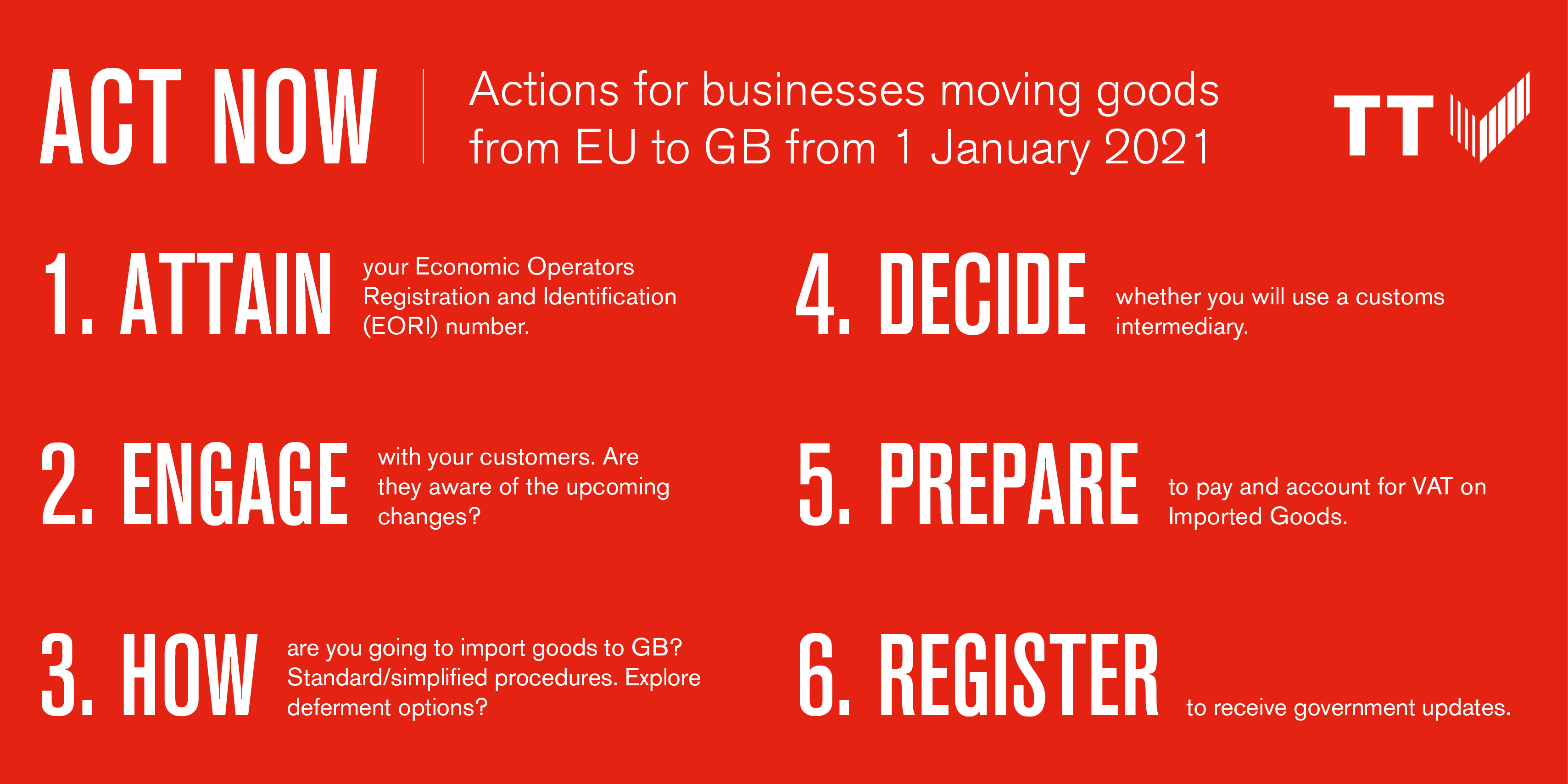

Act now

The necessary steps to take at this stage will differ from business to business and will depend upon the services you intend to provide post 1 January 2021. Whether you are a haulier and your trucks are going to cross borders, a freight forwarder acting as a customs intermediary or a port facility, changes are likely to be required. There are however, no regret decisions that you should now be considering, if you have not already.

- Apply for an Economic Operators Registration and Identification number (EORI or GB EORI if you are based in GB). Find out more at GOV.UK and the European Commission.

Decide if you are going to be offering customs intermediary services. If so:

- Consider training, CHIEF badges, and access to IT systems to make declarations

- Apply for a duty deferment account (DDA) and deferment account number (DAN)

- Verify whether you qualify to use duty deferment without a customs comprehensive guarantee (CCG)

- Prepare for customs declarations; importers and exporters will need to complete customs declarations next year, regardless of whether a free trade agreement is finalised.

- Check VAT guidance to understand your responsibilities and the impact this might have on your cash flow. Consider the need to retain evidence of imported/exported goods.

Engage with your customers:

- Ensure so far as reasonably practicable that they are aware of the upcoming changes and how these might affect their operations.

- Differentiate/identify standard and controlled goods

- Confirm what information/documentation will be required

- Ensure that all commodity codes are identified and verified

- Identify the customs value of the goods

- Verify commercial obligations as outlined in the Incoterms rules, the applicable Incoterm rule in the sales contract will determine required actions

- Verify whether import/export licences are required for their goods

- Consider simplifications or facilitations, such as Customs Freight Simplified Procedures (CFSP's), warehousing, inward processing and transit.

There may be other considerations in the coming months as respective governments provide further clarity, however the above items should be applicable for all, regardless of future negotiations.

At the end of the transition period, the Northern Ireland Protocol (NI Protocol) will take effect. The NI Protocol is a practical solution to avoid a hard border with Ireland whilst ensuring the UK, including Northern Ireland, leaves the EU as a whole, enabling the entire UK to benefit from future free trade agreements. There will be special provisions that apply only in Northern Ireland while the Protocol is in force.

For further guidance regarding the movement of goods after 1 January 2021, please refer to documents below.

We gratefully acknowledge the assistance in the preparation of this article of Mary Prentice, Shoreside Law.

Documents

Border Operating Model (9.41 MB) 08/10/2020

How to export goods from GB into the EU from January 2021 (97 kB) 18/08/2020

How to import goods from the EU into GB from January 2021 (155 kB) 18/08/2020

- Author

- Mike Yarwood

- Date

- 25/08/2020